Publications

Share

Latest publications

World Investment Report 2026: International investment in a turbulent era

World Investment Report 2026: International investment in a turbulent era

Energy transition investment and the transfer of knowledge and skills: Implications for investment treaty design

IIA Issues Note: Energy transition investment and the transfer of knowledge and skills through better

Global Investment Trends Monitor No. 32

KEY MESSAGES:

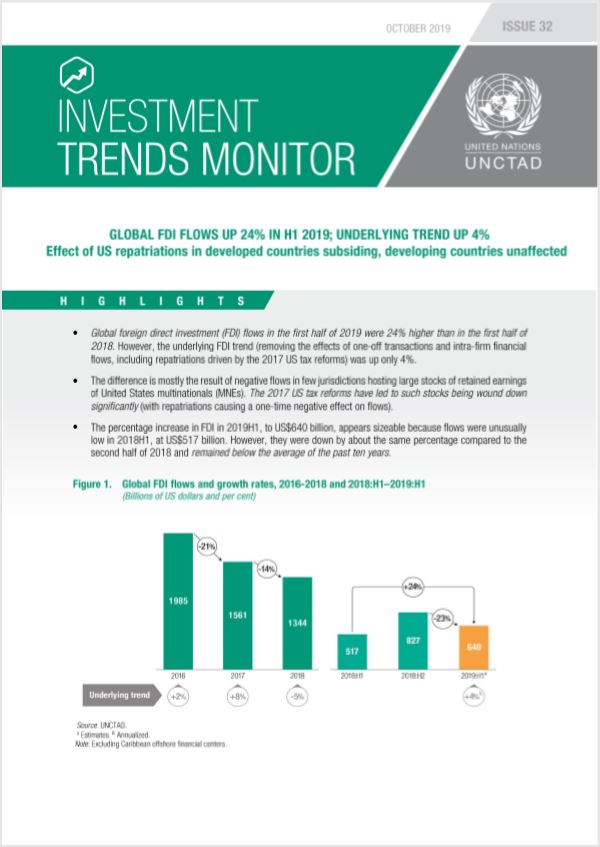

- Global foreign direct investment (FDI) flows in the first half of 2019 were 24% higher than in the first half of 2018. However, the underlying FDI trend (removing the effects of one-off transactions and intra-firm financial flows, including repatriations driven by the 2017 US tax reforms) was up only 4%.

- The difference is mostly the result of negative flows in few jurisdictions hosting large stocks of retained earnings of United States multinationals (MNEs). The 2017 US tax reforms have led to such stocks being wound down significantly (with repatriations causing a one-time negative effect on flows).

- The percentage increase in FDI in 2019H1, to US$640 billion, appears sizeable because flows were unusually low in 2018H1, at US$517 billion. However, they remained below the average of the past ten years.

- Developed economies saw FDI reaching US$269 billion in 2019H1 – almost doubling the anomalously low 2018H1 value. Flows to developing economies, largely unaffected by repatriations, remained relatively stable at an estimated US$342 billion, a decline of 2% compared to 2018H1. FDI flows to transition economies were up 4% from 2018H1 to an estimated US$28 billion.

- Prospects for the full year remain in line with earlier projections of a 5-10% increase. The rebound of flows in developed economies is likely to hold. Developing countries are expected to remain stable, with growth centering on South-East Asia. Weaker global economic activity (with continued downward revisions of forecasts) and ongoing trade tensions form the greatest risk to FDI growth.

- As reported in UNCTAD World Investment Report, GVC-related trade – which is largely driven by FDI – is on a downward trend. Foreign value added, a key indicator, has reached its lowest level in 10 years at 28% of global trade, sharply down from a historic peak of 31% in 2008. New data shows that stagnation in the activity of the global value chains is likely to continue in the coming years.

You can consult the newest SDG Investment Trends Monitor here.